Dear All,

I have a linear programming problem (from a book of optimization in power system) with uncertain parameters as:

max z = 750x1 + 1000x2subject to:

x1 + x2 <= a

x1 + 2x2 <= b

4x1 + 3x2 <= c

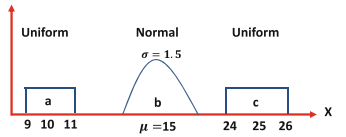

x1,x2 >= 0where a, b, and c are uncertain parameters with the probability function as:

How to implement this optimization problem in AIMMS?

Thank you.

Best answer by FergusHathorn

View original